penelitian kaitan inflasi n kebijakan Fed Fund Rate Conclusion This paper constructs Markov-switching models that estimate the probability of inflation returning to a high-variance, high-persistence regime similar to the 1970s and 1980s, and uses those models to generate prediction intervals around Federal Reserve Board staff forecasts of PCE price inflation. Not surprisingly, the model probabilities show the low-variance regime with a stable mean has governed the behavior of inflation since the 1990s, and as long as the probability of the high-variance, high-persistence regime remains very low, the model’s prediction intervals around one- and two-year ahead forecasts will be well-approximated by those computed from the distribution of forecast errors in the low-variance regime. The paper computes that distribution in the low-variance regime non-parametrically, and shows how to combine that non-parametric distribution with the parametric information from the Markovswitching model. If the model-based probability of the high-variance, high-persistence regime 20For simplicity, estimated shock values are left unrevised. 29 were to increase substantially, the width of the prediction intervals, particularly those using the far tails of the mixture distribution, would widen substantially as well. Additional results in the paper that may be innovations to some information sets include: 1. Over the full 1948-2014 sample, time series evidence strongly suggests the four-quarter inflation measures examined here follow MA(2) processes in differences. On average, about half of the typical innovation to the inflation process reverses after two years, with reversals following large innovations to oil and other commodity prices contributing importantly to this result. 2. Over the last 20 years of the sample, a wide range of evidence suggests there is no random walk component to inflation of any quantitative significance for forecasting purposes. Estimating the probability that a random walk reappears in the inflation process, is, of course, one of the main goals of the paper. 3. Survey measures of long-run inflation expectations, often used to make inferences about whether the current low-variance, low-persistence inflation regime is likely to continue, were unavailable in the late 1960s during the last transition out of such a regime, and were comparatively slow to recognize the transition into the current low-variance regime in the 1990s. The Markov-switching models were much faster in recognizing that regime transition in the 1990s, so they may provide more accurate and timely inferences on regime transitions going forward as well. 4. The tail risks to inflation over the next 5 or 10 years, as measured by financial market derivatives, collapsed in 2014. After that collapse, those measures of tail risks are now much closer to those estimated using the Markov-switching model. 30 5. The Romer and Romer (2000) result that Federal Reserve Board staff forecasts have outperformed their private sector counterparts has not held out of sample, at least for the four-quarter growth rates targeted by the forecasts of FOMC members. Since 1999, Board staff forecasts have been less accurate (as measured by RMSE) than forecasts from both the private sector and the Markov-switching models. The distribution of Board staff forecast errors has taken on a noticeable asymmetry as well: the forecasts at one end of the error distribution, those that were too low, missed by much more than the forecasts at the other end of the distribution that were too high. This asymmetry is largely idiosyncratic to the Board staff—private-sector forecast error distributions or those from impartial models like a random walk or a constant exhibit much less asymmetry—and may stem either from consistent misjudgments about the likelihood that low inflation would persist or from a desire by Board staff to justify loose monetary policy, particularly in 2003, 2004, and in the aftermath of the Great Recession.

bloomberg:

janet yellen Nov 4, 2015:

Inflation Expectation

“If we were to move, say in December, it would be based on an expectation, which I believe is justified, that — with an improving labor market and transitory factors fading — that inflation will move up to 2 percent,” Yellen said.

Michael Gapen, chief U.S. economist at Barclays Capital Inc. in New York, said Yellen’s comments on inflation served to deflect an argument outlined in October by Fed Governor Lael Brainard that the central bank should wait to see movements in inflation before raising rates.

Yellen rejected that argument in favor of a “forecast-based decision,” Gapen said.

“The divide in the committee was essentially over whether they should move in advance of inflationary pressure or wait to see it,” he said. “This clearly says the forecast-based side won that argument.”

congress wants:

Janet Yellen can stay in God’s good graces by waiting until springtime to raise interest rates, Representative Brad Sherman told the Federal Reserve chair on Wednesday.

“God’s plan is not for things to rise in the autumn, as a matter of fact, that’s why we call it fall, nor is it God’s plan for things to rise in the winter, through the snow,” Sherman, a Democrat from California, told Yellen at a hearing of the House Financial Services Committee. “God’s plan is that things rise in the spring. And so if you want to be good with the Almighty, you might want to delay until May.”

Later Wednesday, Sherman wrote on his Twitter account, “Don’t actually think God has an opinion on monetary policy, but if She did, She would agree that the FOMC shouldn’t increase rates in winter.”

At the hearing, Sherman more seriously went on to say that he’s worried about the risks if the Fed lifts off too early and then has to return to zero, among other issues. While his comments were a little more colorful than the typical rationale for postponing liftoff, they underline an important point: Yellen is coming under congressional and political pressure as the Fed inches closer to raising rates.

Yellen said earlier Wednesday that the U.S. economy is performing well and December would be a “live possibility” for a rate increase, though no decision has been made. Rates have been near-zero since 2008 as the Fed tried to encourage economic activity to drive down unemployment and pull inflation closer to its 2 percent goal.

Lobbying Fed

As the central bank prepares to take its foot off the gas, it’s seeing push-back from politicians, non-governmental organizations and interest groups. American Principles Project, a Washington-based non-profit pushing for an increase, held a conference on the sidelines of the Kansas City Fed’s Jackson Hole, Wyoming, summit this year featuring prominent conservative speakers. Fed Up, a coalition of community groups organized by the Center for Popular Democracy in Washington, was also present — but urging for rates to stay low.

While Yellen and her Fed colleagues spend time talking to politicians and groups interested in the central bank’s actions, they’re legally granted independence when setting monetary policy. So Sherman can warn Yellen about Divine wrath, but in the near term, he can’t do much to make sure that she heeds that advice.

marketwatch (04th Nov 2015): U.S. stocks ended Wednesday’s session slightly lower, taking a pause after two straight days of gains.

The main indexes retreated as Federal Reserve Chairwoman Janet Yellen hinted that a 25 basis point rate hike in December would not derail the economy or the housing market. New York Fed President William Dudley also struck a hawkish tone, saying he agreed with Fed Chairwoman that a December rate hike is a live possibility.

Some analysts said the moderate pullback on Wednesday was a function of October’s outsize gains — the biggest monthly climb since 2011.

The S&P 500 fell 7.46 points, or 0.4%, to 2,102.33, with eight of its 10 main sectors closing lower. Energy and consumer discretionary sector stocks were the biggest decliners, while utilities and tech stocks rose modestly.

The Dow Jones Industrial Average fell 50.57 points, or 0.3%, to 17,867.58. The Nasdaq Composite ended the day down 2.65 points, or less than 0.1%, at 5,142.48.

Yellen’s hawkish comments affected traders’ rate-hike expectations, with the odds of a rate hike in December moving to 60% from about 52% on Tuesday, according to the CME Group Fed Watch tool. The yield on the 2-year Treasury note, which is the most sensitive to the prospect of a rate hike, spiked to 0.8%, its highest level in four years.

“Janet Yellen has been signaling a rate hike for a year and markets have already priced in the possibility. Let’s not forget that markets actually rallied after the last Fed meeting when the statement suggested rates would rise in December,” said Bruce Bittles, chief investment strategist at RW Baird & Co.

“We live in a two-tiered economy where manufacturing is slumping but the services sector, which is a much bigger part of the economy is doing well. The slow-growing economy is still the best option for the stock market,” Bittles said.

In economic news, Wednesday’s data came in mixed. A report on private-sector employment showed 182,000 jobs were created last month, while September gains were cut, according to the Automatic Data Processing Inc. Economists look at the ADP report to get a feeling of the official job gains data due on Friday.

“If [jobs] numbers come in near expectations, look for traders to become more convinced that the Fed will finally begin the interest rate normalization process in December,” wrote James M. Meyer, chief investment officer at Tower Bridge Advisors in a note to investors.

Meanwhile, the Institute for Supply Management’s services index rose by more than expected in September to the highest level in three months. The gap between the ISM services and manufacturing indexes is the largest in over 14 years.

The U.S. trade deficit fell in September, but the sharp decline is unlikely to last and give the economy a pop.

The S&P 500 has rallied 13% in just five weeks, noted Michael O’Rourke, chief market strategist at JonesTrading, in a note to investors.

“Most would agree the fundamental situation has not changed much, with exception of a handful of well received earnings reports, which is really no different than any other quarter,” he said.

O’Rourke added that technology, health-care and consumer-discretionary sectors make up more than half of the $1.9 trillion in market capitalization gained during this rally. “It is probably not a good sign if the market is relying heavily on the same narrow leadership,” he said.

Weak US economic data dented confidence on Asian trading floors Wednesday, sending investors running for safe investments ahead of policy announcements by the Federal Reserve and Japan’s central bank.Dealers are nervous heading into the corporate earnings season, with equities and currency markets having suffered their worst quarter for four years during July-September.Analysts warned against reading too much into better than expected sales in China for online giant Alibaba, which came in the face of a growth slowdown in the world’s number two economy.While global markets have enjoyed a broadly healthy run in October on expectations the Fed will delay raising interest rates until next year, another batch of figures indicating a stuttering US economic recovery dampened sentiment.On Tuesday the US Conference Board said an index of consumer confidence fell in September owing to a gloomier outlook for the economy, while the Commerce Department said durable goods orders dipped for a second straight month.The figures come after a Labor Department report at the start of the month showed jobs growth was weaker than expected in September, increasing the chances the Fed will keep rates on hold until the new year.

Wednesday sees its second-last policy meeting before the end of 2015.

“I don’t think the Fed is going to risk tightening policy this year,” Nader Naeimi, the Sydney-based head of dynamic asset allocation at AMP Capital Investors Ltd, told Bloomberg News.

Tuesday’s data also led to losses on Wall Street. The Dow shed 0.24 percent, the S&P 500 dipped 0.26 percent and the Nasdaq eased 0.09 percent.

– Risky currencies fall –

In Asia Wednesday high-yielding but riskier assets were hit.

The dollar climbed against emerging-market units. The Malaysian ringgit fell 0.44 percent and the South Korean won lost 0.05 percent, while New Zealand’s dollar was off 0.51 percent

Australia’s dollar lost one percent against the greenback after inflation in the country remained weak and came in below forecasts, fanning speculation the central bank will cut borrowing costs next week.

But the US unit eased to 120.35 yen, from 120.48 yen in New York and well off the 120.71 yen earlier Tuesday in Asia.

The euro was at $1.1035 and 132.86 yen from $1.1041 and 133.02 yen in US trade. That is well off the $1.1070 and 133.46 yen in Tokyo Tuesday.

The strengthening of the yen — sen as a safe-haven currency — comes before the Bank of Japan’s policy gathering that ends Friday, with pressure on board members to increase stimulus to kickstart the sluggish economy.

Asian equities were also mostly lower, with Hong Kong down 0.58 percent in late trade.

By the close Shanghai had sunk 1.72 percent, hit by worries about the effects of China’s faltering economy on corporate profits.

Sydney ended down 0.21 percent, while Seoul shed 0.10 percent. But Tokyo gained 0.67 percent following a sell-off on Tuesday.

In China Alibaba on Tuesday said online sales surged 28 percent in the three months ended September, while net profit including investment gains rose 36 percent.

However, while the result beat expectations owing to China’s ongoing malaise, Gil Luria, analyst at Wedbush Securities in Los Angeles, said it mostly resulted from the firm’s sales strategy.

“This has little to do with the Chinese consumer but rather Alibaba improving its ability to allow sellers to advertise on mobile screens,” Luria said.

financial post: Mario Draghi is not one to shy away from giving broad hints. While many central bankers have given up on providing any sort of direction to markets — witness the confusion over just about every utterance from U.S. Federal Reserve Chair Janet Yellen — many might find that refreshing. But it doesn’t necessarily make figuring out where global monetary policy is going any easier.

The intertwined nature of exports and capital flows in the modern world forces central bankers of major economies into a close relationship with one another. The global financial crisis last decade forced policymakers to move in lockstep to keep interest rates ultra-low, and Europe, though it was late to the party, eventually got onside — big-time.

But now the banks are starting to diverge. The Bank of Canada seems to be standing pat, the Fed is contemplating when to hike, and Japan and China are still easing. So is the ECB.

The ECB’s main lending rate is as close to zero as dannato is to swearing. Since January, it’s been buying up tens of billions of euros in debt every month as part of its quantitative-easing program. Not surprisingly, European sovereign bond yields are suppressed, and have dipped below zero in some cases (Sweden, Switzerland).

What all this easing is supposed to do is create an incentive for banks, companies and individuals to eschew “safe” debt products and invest in riskier assets, such as stocks. No doubt, the ECB’s QE1 has had some success in the latter regard, with European markets up on the year.

Yet inflation in the eurozone is tracking well below the ECB’s two-per-cent target, and the economic stimulus from its super-accommodative policy has been muted at best.

Draghi’s solution seems to be this: get even more accommodative.

Earlier this week, the ECB decided to maintain its current stance, but Draghi’s remarks gave some broad hints about easing. The ECB head said that come December, the bank would assess the factors contributing to continued deflationary pressure and the options available to address them.

He pointed, in particular, to the QE program’s “flexibility in terms of size, composition and duration.” That was taken as a clear signal that the ECB is prepared to extend QE beyond its planned September 2016 termination — or perhaps even expand it.

Of course, markets loved this hinting, as it suggests that Europe, at least, isn’t going to turn off the lights on the easy-money party just yet. But there may well be another impact of more ECB QE (forgive the alphabet soup) — specifically, on U.S. monetary policy.

No one expects the Fed to raise rates at its next meeting at the end of October, and the markets are pricing in a low expectation of it happening in December. But this expectation is based on the presumption that the Fed is looking not just at the U.S. economy, but also the slowdown in emerging markets and the prospect of a global recession. Yellen said as much in her September statement.

Yet, central-bank moves elsewhere might change that perception. China recently cut interest rates for the sixth time this year and relaxed reserve requirements on banks to stimulate lending. Draghi, meanwhile, seems to be honouring his commitment to do “whatever it takes” to achieve price stability in Europe and encourage economic growth through more money supply and a lower euro.

This puts the ball firmly back in Yellen’s court. How will she address it? It’s quite possible that she won’t.

In other words, the ECB’s move, if it happens, may well take a Fed hike off the table this year, as the U.S. won’t want to risk further strengthening the greenback or triggering a debt crisis in emerging markets.

But there’s another possibility. Easing in Europe and China might give the Fed leave to begin returning rates to “normal” sooner rather than later.

If it looks like other central bankers are handling the problem, then it might just be the hall pass Yellen needs to raise rates based on the domestic economy’s relative strength. (For instance, U.S. jobless claims were down in September, and home sales climbed by almost five per cent.)

The good news for investors is that it could work out well for them either way.

If the Fed holds in December, it will not likely disappoint markets the way it did in September, and the monetary environment will still be easy.

If the Fed hikes in December, it might well be taken as a sign that the U.S. economic recovery is now on a sound footing — which would be good for the Canadian economy — and that the weakness elsewhere is not so severe that other central bankers can’t take care of it themselves.

Either scenario is good for investors, especially Canadian ones in the latter case.

Though some central bankers are (maybe) easing and some are (maybe) tightening, they are creating a monetary environment that should be favourable to equity investors for some time to come.

fortune: The former Fed Chairman says dropping interest rates below zero could help get us out of our next recession.

While the financial world awaits the Federal Reserve’s decision on whether or not to raise interest rates before year’s end, another, perhaps more serious question central bankers are focused on is, What should the Fed do when the next recession comes?

Don’t worry—economists don’t expect another major downturn anytime soon. But even if we don’t see a contraction until 2018, the central bank expects the federal funds rate to only reach 2.6% at the beginning of that year. (It’s been hovering around near-zero since 2008.) And given the fact that the Fed has consistently overestimated economic growth, inflation, and its own ability to raise rates, one could be forgiven for being skeptical that interest rates will even get that high.

And this is what has many economists worried, because historically following recessions, the Fed has had to cut rates much more than just 2.6% to get the economy going again, leaving many worried that the central bank will be out of ammunition to fight the next downturn.

Former Fed Chair Ben Bernanke might have a solution: negative interest rates. In a discussion with Politico’s Ben White at Nasdaq MarketSite on Wednesday morning, Bernanke floated the possibility that the central bank could resort to dropping rates below zero for the first time in history. While the second line of attack against a recession—after reducing interest rates to zero—should be fiscal stimulus, he argued, stimulus is a policy that would not likely receive support from Congress. “If you don’t get that and you get a significant slowdown that requires response, there are things the Fed can do, but none of them are incredibly attractive,” he said.

One of those things is setting interest rates below zero. Economists once believed that a main flaw of using monetary policy to stimulate the economy out of a recession is that rates can’t go below zero, even if the theoretical “market-clearing rate” that gets economy growing again is a negative number. After all, if you start charging people to save money, the thinking goes, people will just start storing cash under their mattresses. But as Bernanke said this morning, “Europe has demonstrated that negative rates are possible.”

Bernanke was referring to recent trials by central banks in Europe, including the European Central Bank, the Bank of Switzerland, and the Danish National Bank, which have all experimented with setting interest rates below what was once thought to be the zero “lower bound.” The Danes have held their overnight rates at negative 0.75% since around 2012, but the effects on the economy have been mixed. According to a recent report in Bloomberg:

Danes have actually been squirreling [money] away. According to central bank data, Danish households’ have added 28 billion kroner ($4.3 billion) to bank deposits since rates shrank to their record low on Feb. 5.

Danish businesses, meanwhile, have barely increased their investments, adding less than 6 percent in the 12 quarters since Denmark’s policy rate turned negative for the first time. At a growth rate of 5 percent over the period, private consumption has been similarly muted.

In other words, negative rates haven’t been the cure-all that some economists had hoped. Then again, 75 basis points below zero isn’t exactly a huge move below where U.S. policy is right now. And banks have been reluctant to pass on the penalties they’ve been paying for keeping their cash parked at the central bank on to consumers and business, although this might be slowly changing.

To engineer interest rates significantly below the rates we’re now seeing, we’d have to change our relationship to paper money. As it stands now, the government guarantees that the nominal return on paper money is at least zero. But if the laws were changed so that paper money was not required to be accepted for “all debts public and private,” and the central bank was allowed to dictate new values of paper money, the Fed could engineer significantly negative interest rates. For instance, if the central bank were able to declare that a person depositing $100 in cash could only be credited $98 when he deposited that money, that would in effect be the same as setting short-term interest rates at negative 2%.

University of Michigan economist Miles Kimball thinks that if governments had the ability to engineer significantly negative interest rates following the recovery, say around negative 4% or more, it would “would have brought robust recovery by the end of 2009.”

These however, are changes that would have to be initiated by Congress and not just the Federal Reserve. But with such figures as Ben Bernanke arguing that the Fed could set rates at least somewhat below zero, it’s not out of the realm of possibility that American consumers and businesses could be charged to save money in the near future.

nnnnnRRRRRnnnnn

the guardian: The US Federal Reserve’s decision to delay an increase in interest rates should have come as no surprise to anyone who has been paying attention to Fed chair Janet Yellen’s comments. The Fed’s decision has merely confirmed that it is not indifferent to international financial stress, and that its risk-management approach remains strongly biased in favour of “lower for longer”. So why did the markets and media behave as if the Fed’s action – or, more precisely, inaction – was unexpected?

What really shocked the markets was not the Fed’s decision to maintain zero interest rates for a few more months, but the statement that accompanied it. The Fed revealed it was unconcerned about the risks of higher inflation and was eager to push unemployment below what most economists regard as its natural rate of about 5%.

It is this relationship between inflation and unemployment that lies at the heart of all controversies about monetary policy and central banking. And almost all modern economic models, including those used by the Fed, are based on the monetarist theory of interest rates pioneered by Milton Friedman in his 1967presidential address to the American Economic Association.

Friedman’s theory asserted that inflation would automatically accelerate without limit once unemployment fell below a minimum safe level, which he described as the “natural” unemployment rate. In Friedman’s original work, the natural unemployment rate was a purely theoretical conjecture, founded on an assumption described as “rational expectations”, even though it ran counter to any normal definition of rational behaviour.

The theory’s publication at a time of worldwide alarm about double-digit inflation offered central bankers exactly the pretext they needed for desperately unpopular actions. By dramatically increasing interest rates to fight inflation, policymakers broke the power of organised labour, while avoiding blame for the mass unemployment that monetary austerity was bound to produce.

A few years later, Friedman’s so-called natural rate was replaced with the less value-laden and more erudite-sounding “non-accelerating inflation rate of unemployment” (Nairu). But the basic idea was the same: if monetary policy is used to try to push unemployment below some pre-determined level, inflation will accelerate without limit and destroy jobs. A monetary policy aiming for sub-Nairu unemployment must therefore be avoided at all costs.

A more extreme version of the theory asserts that there is no lasting tradeoff between inflation and unemployment. All efforts to stimulate job creation or economic growth with easy money will merely boost price growth, offsetting any effect on unemployment. Monetary policy must therefore focus solely on hitting inflation targets, and central bankers should be exonerated of any blame for unemployment.

The monetarist theory that justified narrowing central banks’ responsibilities to inflation targeting had very little empirical backing when Friedman proposed it. Since then, it has been refuted both by political experience and statistical testing. Monetary policy, far from being dissipated in rising prices, as the theory predicted, turned out to have a much greater impact on unemployment than on inflation, especially in the past 20 years.

But, despite empirical refutation, the ideological attractiveness of monetarism, supported by the supposed authority of “rational” expectations, proved overwhelming. As a result, the purely inflation-oriented approach to monetary policy gained total dominance in both central banking and academic economics.

That brings us back to recent financial events. The inflation-targeting models used by the Fed (and other central banks and official institutions such as the International Monetary Fund) all assume the existence of some pre-determined limit to non-inflationary unemployment. The Fed’s latest model estimates this Nairu to be 4.9-5.2%.

And that is why so many economists and market participants were shocked by Yellen’s apparent complacency. With US unemployment at 5.1%, standard monetary theory dictates that interest rates must be raised urgently. Otherwise, either a disastrous inflationary blowout will inevitably follow, or the body of economic theory that has dominated a generation of policy and academic thinking since Friedman’s paper on rational expectations and natural unemployment will turn out to be completely wrong.

What, then, should we conclude from the Fed’s decision not to raise interest rates? One possible conclusion is banal. Because the Nairu is a purely theoretical construct, the Fed’s economists can simply change their estimates of this magic number. In fact, the Fed has already cut its Nairu estimate three times in the past two years.

But there may be a deeper reason for the Fed’s forbearance. To judge by Yellen’s recent speeches, the Fed may no longer believe in any version of the natural unemployment rate. Friedman’s assumptions of ever-accelerating inflation and irrationally rational expectations that lead to single-minded targeting of price stability remain embedded in official economic models like some biblical creation myth. But the Fed, along with almost all other central banks, appears to have lost faith in that story.

Instead, central bankers seem to be implicitly (and perhaps even unconsciously) returning to pre-monetarist views: tradeoffs between inflation and unemployment are real and can last for many years. Monetary policy should gradually recalibrate the balance between these two economic indicators as the business cycle proceeds. When inflation is low, the top priority should be to reduce unemployment to the lowest possible level; and there is no compelling reason for monetary policy to restrain job creation or GDP growth until excessive inflation becomes an imminent danger.

This does not imply permanent near-zero US interest rates. The Fed will almost certainly start raising rates in December, but monetary tightening will be much slower than in previous economic cycles, and it will be motivated by concerns about financial stability, not inflation. As a result, fears – bordering on panic in some emerging markets – about the impact of Fed tightening on global economic conditions will probably prove unjustified.

The bad news is that the vast majority of market analysts, still clinging to the old monetarist framework, will accuse the Fed of “falling behind the curve” by letting US unemployment decline too far and failing to anticipate the threat of rising inflation. The Fed should simply ignore such atavistic protests, as it rightly did last week.

newsweek Updated | In case you hadn’t noticed, interest rates have been at near-zero since the end of 2008, when the entire U.S. economy was facing disaster. This has meant money is cheaper to borrow and it’s given the stock market back its zing.

It has also ushered in some perverse side effects. So hooked are investors on easy money that bad news for the markets is now perceived as good news for them, because it keeps the cheap cash flowing.

Cheap money is a good thing when the economy is struggling to recover. But too much cheap money and the economy can overheat, leading to inflation, bubbles and runaway prices.

That’s why it’s so important for the U.S. Federal Reserve to proceed carefully on exactly when it pulls the rate-hike trigger, which is why its policy-making committee decided not to raise rates when it wrapped up is two-day meeting Thursday. In a statement, the central bank noted that “economic activity is expanding at a moderate pace,” but added that it would keep federal fund rates unchanged and within a target range of between zero and 0.25 percent for now.

At a press conference immediately following the meeting, Fed chairman Janet Yellen emphasized that while the nation’s “recovery from the Great Recession has advanced sufficiently far” to justify discussions of a rate hike, committee members decided not to raise rates in light of low energy prices and a strong dollar putting a “drag” on inflation.

The “outlook abroad has appeared to become more uncertain of late,” she added, amid a China-driven slowdown, plus the Fed wanted to see more progress in the labor market.

For most of the summer, Americans had been bracing for the Fed’s first interest-rate hike in more than nine years—and, until recently, there were strong hints that decision would arrive this month or, at the latest, before the end of the year.

At the press conference Thursday, Yellen emphasized that while inflation remained well below the Fed’s medium-term objective of 2 percent, the drag on the U.S. economy is expected to be “transitory” and the “great majority” of Fed committee members are expecting to vote to hike rates this year—perhaps as early as October.

Only four committee members are projecting a rate hike will be delayed to 2016, she said.

While this afternoon’s announcement was breathlessly billed as Yellen’s “cliffhanger” moment, the verdict was already in from everyday Americans: the economic recovery may be well under way for those who already have plenty of cash in their pockets, but the rest of the country simply needs more time to recoup.

While the stock market is up more than 250 percent since hitting its trough during the Great Recession of 2008-2009, this has not led to an increase in the average American’s paycheck or overall wealth level, which remains effectively wiped out.

Annual data released this week by the U.S. Census Bureau show that even as the nation’s unemployment rate dropped to 5.1 percent in August and the economy posted gains, the median income for middle-class households is unchanged in the fifth year of the economic recovery.

Although Yellen stated that no single data point would determine the timing of a rate hike by the Fed, she repeatedly highlighted the labor market as a critical area for improvement, noting that the labor participation rate is below-trend. In July, the number of Americans over the age of 16 participating in the labor market came in at 62.6 percent—the lowest level on record since 1977 and seen as reflecting the number of Americans who have simply stopped looking for work in a tight market.

The Fed in 2012 agreed to keep interest rates near zero until the unemployment rate fell below 6.5 percent. That gives it a clear path to raising rates now. But the estimated 1.7 million new jobs created so far in 2015 are dwarfed by the number of new university graduates who entered the job market this spring—around 2.8 million.

Meanwhile, 14.8 percent of Americans continue to live below the federal poverty line—well above the pre-recession level of 12.5 percent seen in 2007, according to the latest annual data from the Census Bureau. That’s 47 million people who are still feeling zero effects of the recovery.

Consumer confidence took a hit in September after a brief respite, falling to its low for the year, according to a preliminary report from the University of Michigan. And while energy prices are low, the declines “have not yet increased consumer optimism about the economy,” according to a September survey released this week from the National Association of Convenience Stores, an industry group based in Alexandria, Virginia. “Less than half of all consumers are optimistic about the economy,” it said.

One of the biggest steps to attaining wealth for ordinary Americans is buying a home—a process that has been made somewhat easier in this era of near-zero rates. This summer, Americans raced to buy and refinance their homes, with new mortgage applications climbing more than 20 percent from June to mid-August, says Joel Kan, associate vice president of industry surveys and forecasting for the Mortgage Bankers Association, a Washington industry group. This, certainly, is allowing some Americans to regain a bit of financial footing.

“If you compare this increase to what we saw last year, this has been a better year relative to 2014, when mortgage applications were essentially flat,” Kan tells Newsweek.

The traditionally high-traffic summer buying season hasn’t yielded such strong gains since 2011, according to the MBA’s Market Composite Index, which measures the rate of all new mortgage applications. About half are to refinance homes. And in a sign consumers are acting to take advantage, Kan says about 85 percent of borrowers with a 30-year fixed mortgage are borrowing at a rate less than or equal to 4.5 percent. That’s a good sign for their long-term wealth prospects, even if it’s not showing now.

But even with the summer surge, since mid-August there’s been a marked pullback from those in the market looking for a home or filing to refinance. Ahead of the Fed’s decision, total mortgage applications fell by more than 13 percent for the two weeks ending September 11.

Last week’s drop of 7 percent alone was the biggest in more than three months—although Kan notes it was likely affected by the Labor Day holiday. The biggest one-week drop in 2015 was just over 13 percent in mid-February.

All of which sends another signal that America’s recovery may still be dependent on rates staying low.

How the central bank proceeds in the coming weeks will be very instructive in revealing how much it weighs the plight of ordinary Americans against the resurgence of Wall Street. Yellen says the Fed expects to see unemployment decline to its lowest sustainable level sometime in 2016 before “leveling out,” according to committee members’ median estimates, while inflation isn’t expected to reach the Fed’s 2 percent objective until 2018.

As Republican presidential contender Jeb Bush emphasized during the GOP debate last night, much more hangs in the balance than markets and mortgages. He went so far as to link American prosperity with its fate as a superpower, stating, “Without a high-growth strategy, our country will never have the resources or the optimism to lead the world.”

This story has been updated after the Fed’s decision to hold rates unchanged with comments from Janet Yellen explaining the decision

Jobless Rate Falls to Lowest Since the Recovery Began

Chris Matthews / Fortune

Yet we are seeing no recovery in wage growth or labor force participation

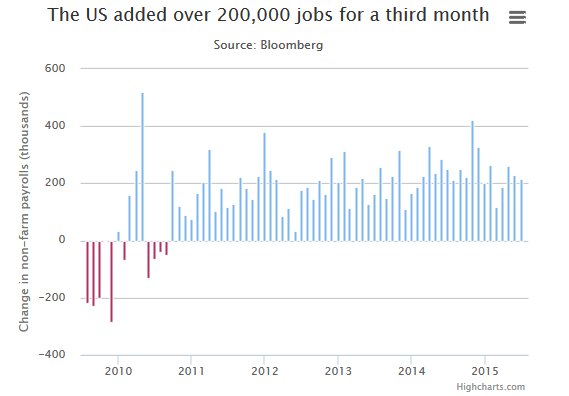

The U.S. economy added 173,000 jobs in August, while the unemployment fell to 5.1%, according to a report released Friday by the Labor Department.

The total number of new non-farm payroll jobs was about 50,000 lower than economists had expected, but that was tempered by the fact that estimates for job gains in June and July were revised up by a total of 44,000 jobs.

The unemployment rate, now at 5.1%, is now at the lowest rate since April of 2008, well before the beginning of the economic recovery. While that sounds like great news, much of that decline can be blamed on the fact that the labor force participation rate, or the ratio of folks in the labor market to Americans over the age of 16, remains at levels not seen since the late 1970s, before women began entering the job market in force.

More: 3 Ways Friday’s Jobs Report Could Affect Interest Rates

Another reason for concern: the report shows no sign that workers are getting a significant raise. Average hourly earnings have increased just 2.2% over the past year, while there’s evidence that much of these increases are being captured by more elite workers. As Daniel Alpert, Managing Partner of NY investment bank Westwood Capital tweeted:

In other words, this jobs report doesn’t tell us much about the economy we didn’t already now. We’re still adding a healthy number of jobs each month, but we’re still seeing no signs of the strong wage growth that would both move the economy back towards 2% inflation, or spur the kind of above-trend economic growth that we once saw following recessions.

Liputan6.com, Jakarta –Dana Moneter Internasional/International Monetary Fund (IMF) mengatakan bank sentral Amerika Serikat/ The Federal Reserve memiliki kesempatan untuk menunda menaikkan suku bunga di tengah gejolak ekonomi global.

“Pandangan umum kami adalah bahwa mereka (The Fed) memiliki fleksibilitas untuk menunda,” kata juru bicara IMF William Murray, seperti dikutip dari The Telegraph, Jumat (4/9/2015).

Murray juga mengatakan The Fed “sebaiknya memproses secara bertahap” sesuai dengan prosedur kenaikan suku bunga tersebut. Murray menambahkan ekpektasi atas rencana kenaikan suku bunga oleh bank sentral di negara seperti Amerika Serikat, dan Inggris berdampak pada meningkatnya pertumbuhan ekonomi mereka. Murray menyarankan masih ada waktu untuk menunggu sebelum mengambil langkah pertama.

“Situasi global cukup bergejolak. Pandangan IMF adalah The Fed “sebaiknya memproses secara bertahap” kata Murray.

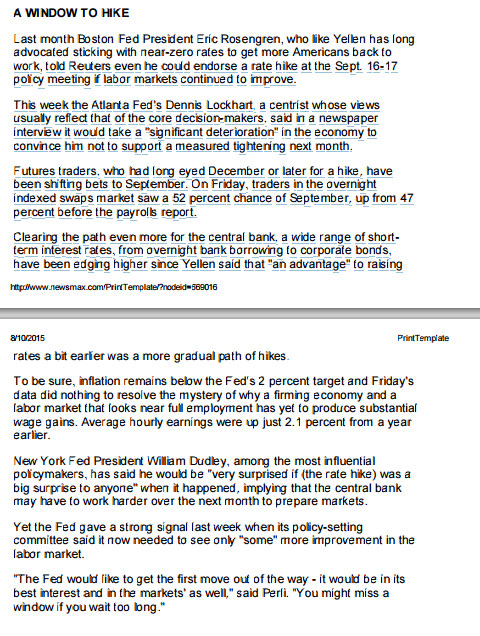

The Fed telah mempertahankan suku bunga acuan mendekati nol sejak 2008 dengan tujuan memulihkan perekonomian pasca krisis ekonomi. Para pimpinan The Fed dijadwalkan bertemu pada 16-17 September 2015. Murray melihat inflasi AS dan tekanan upah, adalah dua barometer kunci untuk menunda kenaikan suku bunga.

Artinya bank sentral AS “mampu mempertahankan suku bunga rendah hingga ada tanda-tanda yang lebih jelas dari tingkat upah atau tingkat inflasi saat ini”.

Murray mengatakan, penundaan kenaikan suku bunga AS sangat penting bagi sebagian besar negara lain di dunia ini untuk dapat menyesuaikan keadaan. Harapan atas kenaikan suku bunga AS telah memicu arus modal keluar dari negara negara berkembang, sehingga menyebabkan mata uang negara tersebut jatuh. (Ilh/Ahm)

WASHINGTON (AFP) – Federal Reserve vice-chairman Stanley Fischer warned Saturday that the US central bank will not wait for inflation to hit two percent before raising interest rates.

In a speech at a conference on monetary policy in Jackson Hole, Wyoming, the Fed’s No. 2 said: “We should not wait until inflation is back to two percent to begin tightening.”

He added, however, that the Fed needed to “consider the overall state of the US economy as well as the influence of foreign economies on the US economy as we reach our judgment on whether and how to change monetary policy.”

Fischer said he was confident that US inflation was on track to meet the 2 per cent target that the Fed considers a sign of a healthy economy, even though changes in the personal consumption expenditure index “have recently been only above zero” due to temporary factors like declining oil prices.

According to the PCE index, consumer prices currently are only up 0.3 per cent over the past year, notably because of low oil prices but also because of easing demand in China and elsewhere.

The Fed’s projections put core inflation, excluding oil and food prices, at between 1.6 and 1.9 per cent next year, rising from 1.2 per cent in July.

Among the factors keeping inflation low, Fischer cited the 17 per cent increase in the value of the US dollar since last summer which has lowered prices of imports.

He added it was “plausible to think that the rise in the dollar over the past year would restrain growth of real GDP through 2016 and perhaps into 2017 as well.“

Evoking the impact of the foreign economic situation on US growth, Fischer explicitly mentioned China, departing from the Fed Open Market Committee’s usual language making oblique reference to “international developments.”

“At this moment, we are following developments in the Chinese economy and their actual and potential effects on other economies even more closely than usual,” Fischer said.

The Fed’s Open Market Committee is scheduled to meet Sept 16 and 17 and most economists believe that it will begin to raise interest rates, which have been at near zero since the 2008 financial crisis.

But turbulence in the financial markets in recent weeks in the wake of the slowing of the Chinese economy has raised doubts about the timing of such a move.

bloomberg: The third time inflation has fallen to zero in Japan this year persuaded some market watchers that Abenomics needs to be taken back for an overhaul.

The government will be forced to delay an increase in the sales tax scheduled for April 2017 and the Bank of Japan won’t be able to taper its unprecedented bond buying as envisaged, according to Sumitomo Mitsui Banking Corp. Only one economist in asurvey by Bloomberg from July 27 to Aug. 3 said inflation would reach the BOJ’s goal in its target six-month period through September 2016. A majority of the 37 respondents see the BOJ boosting monetary stimulus.

China’s economic slowdown, tumbling oil prices and a rally in the yen are all conspiring against Governor Haruhiko Kuroda’s effort to reflate the world’s third-biggest economy. While more BOJ bond buying would keep government yields close to record lows, any delays in overhauling taxes and reviving growth raise the risk of a rating downgrade for Japan, which has the world’s biggest sovereign debt burden.

“Deflation is the biggest problem for Japan,” Junko Nishioka, the chief economist at Sumitomo Mitsui, the nation’s second-biggest bank by market value, said in an interview on Aug. 26. “We are entering a difficult phase of balancing the BOJ’s inflation target, Japan’s second sales tax hike and sustaining global economic growth. A delay could prompt a ratings downgrade.”

Consumer prices excluding fresh food were unchanged in July from a year earlier, the Statistic Bureau said on Friday. The bond market is signaling that inflation will average around 0.9 percent in the next 10 years, below the BOJ’s 2 percent target, according to the so-called break-even rate.

Japan wants to cut a debt burden that is more than twice the size of economic output, without damaging growth by moving too rapidly with spending cuts or tax increases. A sales-levy hike in April 2014 pushed the nation into a recession and prompted Prime Minister Shinzo Abe to postpone another planned increase until April 2017.

“The fundamental problem is that Japan’s government is struggling to both reflate the economy and establish a semblance of fiscal credibility,” Nicholas Spiro, managing director at advisory firm Spiro Sovereign Strategy, wrote in an e-mail on Aug. 27. “It’s the worst of both worlds: no meaningful growth and no credible fiscal consolidation.”

Japan’s debt is unsustainable and could climb to almost three times the size of its economic output by 2030 unless the government does more to cut its budget, according to the International Monetary Fund. The nation’s primary budget deficit will be 6.2 trillion yen ($51 billion) in the year starting in April 2020, smaller than a projection in February but still not the surplus the government is aiming for.

Global Risk

Stocks worldwide tumbled last week amid concerns that China’s economic slowdown will jeopardize global growth. The Japanese government cut its assessment on the global economy for the first time since August 2012 last week, citing weakness seen in some areas such as Asian emerging nations.

“Fiscal constraints keep Japan’s reliance on unprecedented monetary easing and that’s likely to continue and make tapering quite difficult,” said Tsuyoshi Ueno, a senior economist at NLI Research Institute in Tokyo. “The economy needs support to weather the sales-tax hike impact while concerns about China weighing on growth may raise pressure against the tax hike.”

The benchmark 10-year Japanese government bond yield has been on a declining trend over the past 20 years despite the nation’s growing debt, driven in part by the central bank’s accommodative policy. The notes, predominantly owned by domestic investors, yielded 0.38 percent late Friday after plunging to a record low of 0.195 percent in January.

Demographic Challenge

“Yields would normally climb if the market sees a retreat in the fiscal rebuilding policy, but if the economy is so bad that the sales tax can’t be raised, monetary easing will need to be prolonged,” said Ueno. “An exit from the current unprecedented stimulus is nowhere in sight.”

Japan also faces demographic challenges, Sumitomo Mitsui’s Nishioka said. Social welfare took up about a third of the budget this fiscal year in one of the fastest-aging nations in the world, while debt redemption and interest payment costs made up 24 percent, according to Finance Ministry figures.

A bright spot for the economy is that Abe’s reflationary policies have boosted corporate profits to a record, leading to the highest tax revenue since fiscal 1993 last year.

“Japan faces ballooning social security costs with the aging and shrinking population,” Nishioka said. “That means it’s essential for the government to bolster inflation and nominal tax revenue through monetary easing to enable financing the pension and medical expenses in the future.”

9:00PM BST 19 Aug 2015

The Telegraph, UK

Monetary policymakers in the US are looking for stronger signs of an improving economy before deciding to hike interest rates for the first time in nine years.

Federal Reserve policymakers said the conditions for a rate hike were now “approaching” but were looking for further signs of a rise in inflation, in the latest set minutes from their July policy meeting.

“Almost all members” of the committee “indicated that they would need to see more evidence that economic growth was sufficiently strong” before voting in favour of rate hike, said the transcript of a cautious set of minutes.

Only one policymaker was ready to vote for a rate hike last month, while a number of others “viewed the economic conditions for beginning to increase the target range for the federal funds rate as having been met or were confident that they would be met shortly”.

• Bank of England or Federal Reserve: Who will move first on interest rates?

Financial markets are now pricing in a 40pc probability that rates will be hiked from a record low range between 0pc and 0.25pc at the committee’s (FOMC) next meeting in mid-September. The FOMC however made few indications of the timing of the lift-off.

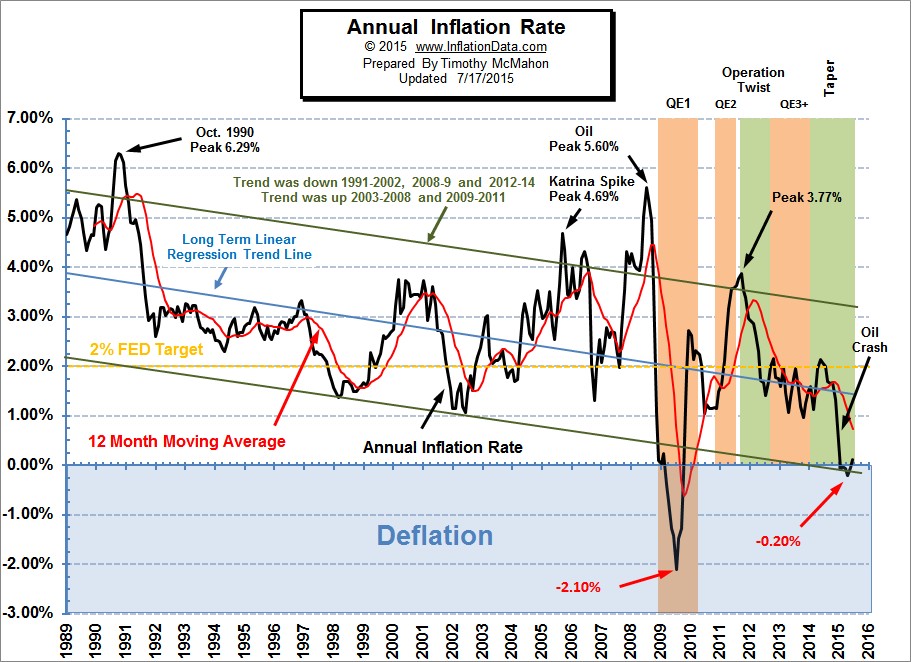

The minutes were released as consumer prices rose by a modest 0.1pc last month. The uptick in inflation was slightly lower than analyst forecasts of 0.2pc , and will give the Federal Reserve “pause for thought” over a September rate rise, said Paul Ashworth, chief US economist at Capital Economics.

“The decision is finely balanced. With underlying price inflation and wage growth still muted, a case can also be made for waiting,” said Mr Ashworth.

A measure of core inflation, which strips out volatile elements such as food and energy, rose by 1.8pc in the year to July. But world’s largest economy could still fall into deflation in the coming months, said Josh Mahoney of IG.

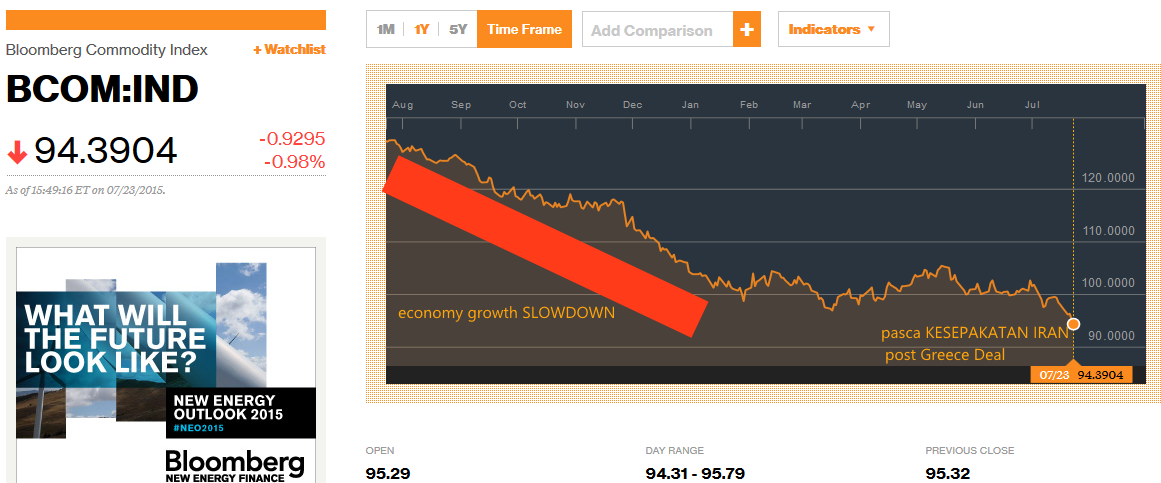

“The impact of multiyear lows in commodity prices and a likely continued depreciation of the yuan” could drive the US economy back into negative prices, he said.

With the Fed keeping a close eye on the labour market, robust job creation could also edge it to move towards a normalisation of monetary policy. The US economy added 215,000 jobs in July, with the minutes noting that labour market improvements are nudging the FOMC towards a rate hike sooner rather than later.

http://cloud.highcharts.com/embed/isebew

The July meeting took place before recent moves by the People’s Bank of China to devalue the renminbi, sparking a fresh round of stock market volatility. The minutes revealed that fears of an “adverse spillovers from slower economic growth in China raised some concerns”.

10:18 am ET

Jun 1, 2015

economics

Inflation Misses Fed’s 2% Target for 36th Straight Month

It’s been three years since U.S. inflation hit the Federal Reserve‘s 2% target, according to new data from the Commerce Department.

The personal consumption expenditures price index, the Fed’s preferred inflation gauge, rose just 0.1% in April from a year earlier, the lowest level since October 2009 and a little softer than the 0.3% reading in February and March.

April 2012 was the last time the inflation rate was on target. That’s the longest such stretch of sub-2% inflation since the 1960s.

Excluding the volatile food and energy categories, prices climbed 1.2% in April from a year earlier, a slight downshift from the 1.3% reading the prior four months.

Such low inflation complicates the Fed’s plans to start raising interest rates. The central bank’s dual mandate calls for price stability–in this case 2% inflation–and maximum employment. While the labor market appears healthy, low oil prices, a strong dollar and tepid global demand are all holding down prices.

“It won’t be current inflation that prompts the first Fed hikes, it will be the tightness of the labor market and the signal it sends about future inflation risk, given the extraordinarily easy stance of policy,” Ian Shepherdson, chief economist at Pantheon Macroeconomics, said in a note to clients.

Commodity Prices and Inflation: Evidence From Seven Large Industrial Countries

James M. Boughton, William H. Branson, Alphecca Muttardy

NBER Working Paper No. 3158

Issued in November 1989

NBER Program(s): EFG ITI IFM

This paper examines the relationships between movements in primary commodity prices and changes in inflation in the large industrial countries. It begins by developing a two-country model in order to examine the theoretical effects of monetary, fiscal, and supply-side disturbances on commodity and manufactures prices and on exchange rates.

It is shown that if monetary shocks dominate, then commodity prices should lead general price movements, and the level of commodity prices should be correlated with the general inflation rate.

Non-monetary shocks generally weaken these relationships, but such disturbances may cancel out for broad indexes covering a wide range of commodities.

Country-specific commodity price indexes are developed for the major industrial countries. The weights assigned to different commodities vary substantially across countries. Nonetheless, when the indexes are expressed in a common currency, they tend to be highly correlated over time, except when sharp movements occur in certain commodity prices. The major source of contrast across countries in the behavior of the indexes derives from exchange rate movements.

Several empirical tests broadly support the conclusions of the theoretical model, with relatively few differences across countries. Three main tendencies may be cited. First, low inflation in industrial countries has tended to be associated with low levels of commodity prices, and conversely; commodity-price levels are cointegrated with consumer-price inflation rates. Second, there has been some tendency for movements in commodity prices to precede changes in general inflation rates by a few months, although it is not clear whether this tendency is strong enough to be a reliable aid in forecasting the rate of inflation. Third, there is a strong and fairly reliable tendency for turning points in general inflation rates.

Commodity prices thus appear to contribute to predictions of turning points in inflation, predictions of inflation rates but more strongly to predictions of turning points in inflation.

SEPTEMBER, the month: