Eyeing a Mercedes-Benz? Those looking for an A-, B-, C-, CLA- and S-Class can now enjoy the benefits of Agility Financing, an innovative hire purchase based instalment plan by Mercedes-Benz Services Malaysia (MBSM). The scheme is the first-of-its-kind to guarantee the future value of your car.

“Our Hire Purchase Agility has received positive response from customers since it was first introduced in 2013 with the launch of the new E-Class. This is an excellent indicator that our financing solutions are aligned to the needs of our customers, and this has motivated us to give customers more choices,” said MBSM’s MD Hilke Janssen.

With Agility Financing’s flexible and affordable features now made available to more models, MBSM is tapping into a wider customer profile which ranges from young professionals, families and senior professionals.

Guaranteed Future Value sample based on 10% downpayment, 60-month tenure – click to enlarge

Customers will enjoy the risk free benefits of Guaranteed Future Value (GFV) and have full control over the decision to settle the financing, extend an agreement or simply return the vehicle to Mercedes-Benz at the end of the tenure. The return feature suits the lifestyle of customers who wish to change cars regularly without the hassle of selling.

To learn more about how Agility Financing works, visit www.mercedes-benz.com.my/agility or download the myMBFS app from Apple’s App Store and Google Play. Also check out carbase.my for full specs and details.

Looking to sell your car? Sell it with Carro.

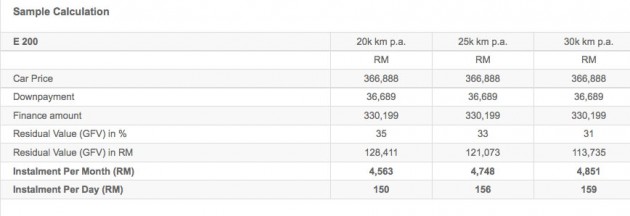

Based on the calculation, does it mean that to own a E200 for 5 years for 100K KM, what I need to pay is just RM36,689 as downpayment, and RM4,563 per month. After 5 years, I can just return the car to MB, and everything will be settled? That will total up to RM310,469 over 5 years, excluding maintenance.

You are quite right. But I think it also means that after 5 years, upon returning your car to Mercedes Benz, you will get back the GFV of RM128,441.

Correct me if I am wrong…

No, you don’t get back any money. You have to pay off the GFV if you want to keep the car, else you just hand over the car back to MBM.

“End of Agreement Options

Settle: Pay the remaining residual value and take full ownership of the car.

Extend: Extend your agreement by refinancing the residual value.

Return: Hand back the keys with no further obligations – other than any excess kilometre charges and and subject to fair wear and tear.”

In short, you are leasing the car for 5 years and if you return the car that is the end. Very expensive and not practical for private owners and only suitable for companies.

Suitable for those who keep changing cars after 5 years too. Safe you the hassle of reselling.

The GRV will give you the option to get a FIRM value of you sell the car back to MBM and pick up another new or approved MB car. Since the car mileage is still relatively low and top top shape, MB can sell these approved cars to the market rather easily and compete with recon cars without warranties being brought in by the AP kings thus enabling MBM to compete with they grey importers, one thing I like is that the amount of interest you pay to MBM is much lower than banks if u take 3 year loan since interest is charged only on the 3 years financing as compared to a typical bank loan that stretches from 5 to 9 years , with this conventional loans , the banks would have already made maximum profit out of the loan during half the tenure and rebates are very little of you settle earlier than the loan period.

Yes. You are right. By the end of your tenure, return your car and end of story. Maintenance on your own.

what i understand from the description is that at the end of the tenure, we have the option of:

1. get full ownership of the vehicle by paying off the remaining amount.

2. extend the tenure by refinancing the remaining amount, i.e. the same instalment applies.

3. just hand it back to mercedes.

i would prefer the 2nd option, i.e. refinancing the the remaining amount.

bwk je protong kalo uang xde…buatpe nk berlagak

I’m sorry to say, that’s why people like you will never improve.

Good luck to you, forever driving potong.

haha, oh, yeah…I don’t have the habit of showing off…and it’s not safe to drive such car in this country anyway.

xXx speak like a loser in life. No money still want to talk cock. You can get robbed even when you are walking on the road. Cannot afford then shut up. Don’t make moronic statements in Paultan.org. Whether people buy cash, finance or agility program they are driving and enjoy the prestige of the three pointed star.

Con job.

After 5 years, only guaranteed thus little. Might as well sell in open market and you may get even better.

Talk so much and beat around the bush. Isn’t this just a lease?

now my macai can drive marseelee

Why would any one go for this plan?

Assuming you take up a loan from a bank with a MOF at 90% at 2.8% pa for 5 years.

Purchase Price : RM 366,888.00

Downpayment : RM 36689.00

Finance Amt : RM 330199

Instalment per mth : RM 4481.27

Based on the above scenario, why would one opt for MBSM’s financing options?

Isnt it better to stick with the conventional financing where at the end of 5 years you get to own the car without having to pay for the GFV to own the car and furthermore the instalment per month is less than MBSM’s option?

Besides, one can still sell the car for easily more or less around RM 150 k after the 5 years.

Correct me if i am wrong.

Assuming you take up a loan from a bank with a MOF at 90% at 2.8% pa for 5 years.

Purchase Price : RM 366,888.00

Downpayment : RM 36689.00

Finance Amt : RM 330199

Installment per mth : RM 6273.78 (not 4481.27)

You have to finance the car for 7 years to get monthly repayment of RM 4701.40, which is close to RM 4481.27

Only left with 30% residue future value after 5 years ! Must be targeting the soon to be retirees in the next 5 years.

It is just leasing in disguise. Good for companies and MLM people.

Correct me if i am wrong but it should work out like this

RM4563x60 = RM273k

so after five year you return the car to MBM and as mention there would be a GFV of RM128k so it will be RM273k – RM128k = RM145k

So you will be losing around RM145k for owning the Merc for 5 years without the hassle selling off the car urself….

This is similar to all those lease financing package widely avail in Europe. Doesn’t work for everyone, mind you, esp with Malaysian mentality of “mesti” own the car by end of financing. This works for people who clocked low mileage annually(only drives in town or car rarely moves on weekly/monthly basis) and prefers to change to new car every 5 years. Won’t work for people who can only afford 9 years loan(and take 100% margin loan) or take 3-5 years loan only but drives the same exact car for the next 15 years.

No need to bash or comment why conventional hire purchase loan is better or cheaper. People buy cars for various reason with different goals and wants at the end of the day. If it doesn’t work for you financially, just ignore and take conventional hire purchase.

Disclaimer: I am not Mercedes Benz Sales Advisor LOL

Assuming you take up a loan from a bank with a MOF at 90% at 2.8% pa for 5 years.

Purchase Price : RM 366,888.00

Downpayment : RM 36689.00

Finance Amt : RM 330199

Installment per mth : RM 6273.78

Total 5 years Payment:

RM6273.78x12x5 + RM 36, 689.00= RM413115.8

Based on the calculation, does it mean that to own a E200 for 5 years for 100K KM, what I need to pay is just RM36,689 as downpayment, and RM4,563 per month. After 5 years, I can just return the car to MB, and everything will be settled? That will total up to RM310,469 over 5 years, excluding maintenance.

COMPARE::

RM413,115 vs RM310,469

difference = RM100k

use own scheme, just need RM100,000 extra to own the car for life. Use BEnz’s scheme, Save RM100,000, own for 5 years.

furthermore, 5years old E300 worth RM200,000 now

If at the time of “surrender” the market price is higher than the FGV, just sell it to the market, and use the differential as your deposit for your next MB.